Content

Under the 2021 FAQ Question 15 exception, the key date was the date the return was filed by the partnership, so that any notice of a need for the information prior to the actual filing of the return meant the exception was not met. If any portion of profits were paid out to owners beyond their standard guaranteed payments, or if you paid anyone outside the partnership more than $600 to do contract work and filed a Form 1099, you’ll have to report this information on your 1065 as well. To file Form 1065, you’ll need all of your partnership’s important year-end financial statements, including a profit and loss statement that shows net income and revenues along with all the partnership’s deductible expenses__, and a balance sheet for the beginning and end of the year. This language is provided for your consideration and may be useful in notifying shareholders or partners of business entity returns you are preparing. You may wish to review the letter and the Schedule K-1 language with your attorney. We do not practice law and make no representations of their legal status or viability.

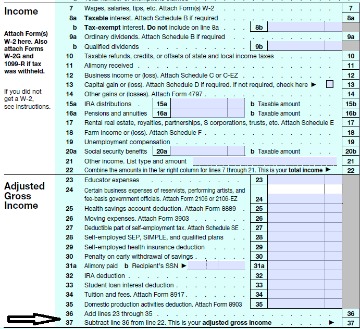

You cannot claim any payment for, or reimbursement of, a moving expense actually deducted by you in a prior year. Federal law requires holders of stock or indebtedness in a federal S corporation to include undistributed taxable income in their federal adjusted gross income and take a corresponding increase in basis. If you are a shareholder of an S corporation which is a New York C corporation, then enter any S corporation pass-through items of loss or deduction you took into account when you computed your federal adjusted gross income, pursuant to IRC section 1366. If you deducted special additional mortgage recording tax when you computed your federal income, and you paid the special additional tax before January 1, 1988, and in a prior year, you were allowed a New York State personal income tax credit for that tax, then enter the amount deducted. If, during the tax year, any interest or dividend income from any U.S. government authority, commission, or instrumentality that federal laws exempt from federal income tax but do not exempt from state income tax was received or credited, then enter that income. If you are uncertain whether a particular federal bond or obligation is subject to state income tax, contact the Tax Department.

How To Fill Out Form 1065: Overview and Instructions

If you are subject to the special accrual rules, then enter your accrued item of income, gain, loss, or deduction. Enter the subtraction modification on line 30 of Form IT-201, as applicable. Partners, shareholders, and beneficiaries—Do not complete Form IT-399 to determine the amount to enter. Include applicable amounts from all existing accounts owned on lines 1 through 7 of the worksheet below. Do not include amounts applicable to accounts that were closed in a prior tax year. If you are filing a joint return, include the applicable amounts from all existing accounts owned by you and your spouse.

The Schedule K-1 is the form that reports the amounts that are passed through to each party that has an interest in the entity. These businesses are often referred to as pass-through entities. If the business needs an extension, it must file Form 7004 by the appropriate deadline for its tax year. When filed by the deadline, the company automatically receives a six-month extension. The IRS won’t contact the business with approval, but it will if the extension is denied.

Tax Forms

K-1 income generated from an S Corp where you materially participate is considered non-passive income. It is not necessarily earned income and it is not passive income. It is something in between, but definitely without the Social Security and Medicare tax element. Nonprofit religious organizations classified as 501 also file this form. They must show that profits were given to their members as dividends, regardless of whether they were distributed.

- A requests Schedule K-3 from USP for tax year 2022 and USP receives this request on February 1, 2023.

- If this balance sheet differs from the one in your company’s financial statements, you’ll need to attach a statement explaining the discrepancies.

- Assets of decedents can sometimes have different bases for state and federal tax purposes.

- When filed by the deadline, the company automatically receives a six-month extension.

- Form 1065 is also used by limited liability companies with more than one member to file their federal income tax return.

Generally, this combination is used to compute a net cost recovery deduction that is reported on Line 1. PTPs will generally be unable to compute amount of income or deductions related solely to IRC Section 743 adjustments, as required by this reporting change. The Draft Instructions do not provide an exception to the requirement to report the partners’ shares of net unrecognized IRC Section 704 gain or loss for publicly-traded partnerships . This new item requires disclosures regarding IRC Section 704 items on an ongoing basis — not merely when built-in-gain or built-in-loss property is contributed by a partner to a partnership. Furthermore, this new requirement appears to implicate “reverse” IRC Section 704 layers.

What is a payment gateway?

With respect to a partnership that satisfies criteria 1 and 2, partners receive a notification from the partnership either electronically or by mail dated no later than 2 months before the due date for filing the partnership’s tax year 2022 Form 1065. The notification must state that partners will not receive Schedule K-3 from the partnership unless the partners request the schedule. As referenced previously, PTPs generally rely upon the combination of the remedial method and IRC Section 743 adjustments to allow for fungible income allocations to their partners.

A domestic or foreign publicly traded partnership as defined in section with no foreign activity or foreign partners may need to complete Part XI. See each part for applicability. The purpose of Schedule M-2 is to inform the IRS of any changes to you or your partner’s capital accounts in the form of cash, property or any other capital contributions. Even if there are no differences between book income and reported income, a partnership that does not meet all four requirements in part 6 of Schedule B must file Schedule M-1. If your partnership does not meet all four requirements in part 6 of Schedule B—for example, if your partnership’s total annual receipts are more than $250,000 or its assets are more than $1 million—then you must fill out Schedules L, M-1, and M-2.

What happens if you dont report k1?

Instead, the individual and LLC members complete a Schedule K-1 to report their share of the business’s profits and losses and then file this form with their personal tax returns . Florida corporate income/franchise tax is computed using federal taxable income, modified by certain Florida adjustments, additions, and subtractions, to determine adjusted federal income. If you received any grant, pursuant to the COVID-19 pandemic small business recovery program irs 1065 instructions established in the New York State Urban Development Corporation Act, § 16-ff, then enter the amount of the grant, to the extent you included them in your federal adjusted gross income. If you received a health care and mental hygiene worker bonus payment under social services law section 367-w or under section 4 of part ZZ of Chapter 56 of the Laws of 2022, then include the amount of the bonus payment to the extent it was included in federal gross income.

What is Form 1065 Schedule M 1?

In Form 1065, U.S. Return of Partnership Income, Schedule M-1 is used to reconcile the income that the partnership is reporting on the tax return with the income in its accounting records. Not all partnerships are required to complete Schedule M-1.

Schedules L and M-1 contain items that will have to match items on M-2, so make sure to fill those out first before filling out M-2. If the entity elects to extend the due date until September 15, 2023, then the deadline in the last paragraph needs to be changed to August 15, 2023. This site is brought to you by the Association of International Certified Professional Accountants, the global voice of the accounting and finance profession, founded by the American Institute of CPAs and The Chartered Institute of Management Accountants. In this Journal of Accountancy podcast, learn how to better understand the ins and outs of these formidable forms.